The AIEOG AI Lexicon Explained: Key Terms Every Community Bank Should Know

In February 2026, Treasury's AIEOG released an official AI Lexicon and Risk Management Framework for financial services. Here are the terms that matter most for community banks — and what they mean in practice.

TL;DR

In February 2026, the U.S. Department of the Treasury released an official AI Lexicon for the financial sector, developed through the Artificial Intelligence Executive Oversight Group (AIEOG), a public-private partnership between Treasury, FBIIC, and FSSCC. The Lexicon establishes a shared vocabulary for AI concepts, capabilities, and risk categories. This post explains the terms most relevant to community banks, groups them by topic, and connects them to the Financial Services AI Risk Management Framework (FS AI RMF) released alongside it.

Community bank compliance officers, COOs, and technology leaders are increasingly expected to have informed conversations about AI, not just with internal staff but with regulators, examiners, and third-party vendors. That conversation has historically been difficult because the terminology has been inconsistent. One vendor's definition of AI governance does not match another's. Examiner language has differed from industry language. Internal staff and external providers have been talking past each other using the same words.

The AIEOG AI Lexicon addresses this directly. Released February 19, 2026 by the U.S. Department of the Treasury through the Artificial Intelligence Executive Oversight Group (AIEOG), it establishes shared definitions for AI concepts across regulatory, technical, legal, and business functions in financial services. The Lexicon is not a regulatory requirement. It is a reference tool, and it is the vocabulary that regulators, examiners, and industry participants are increasingly using when they talk about AI.

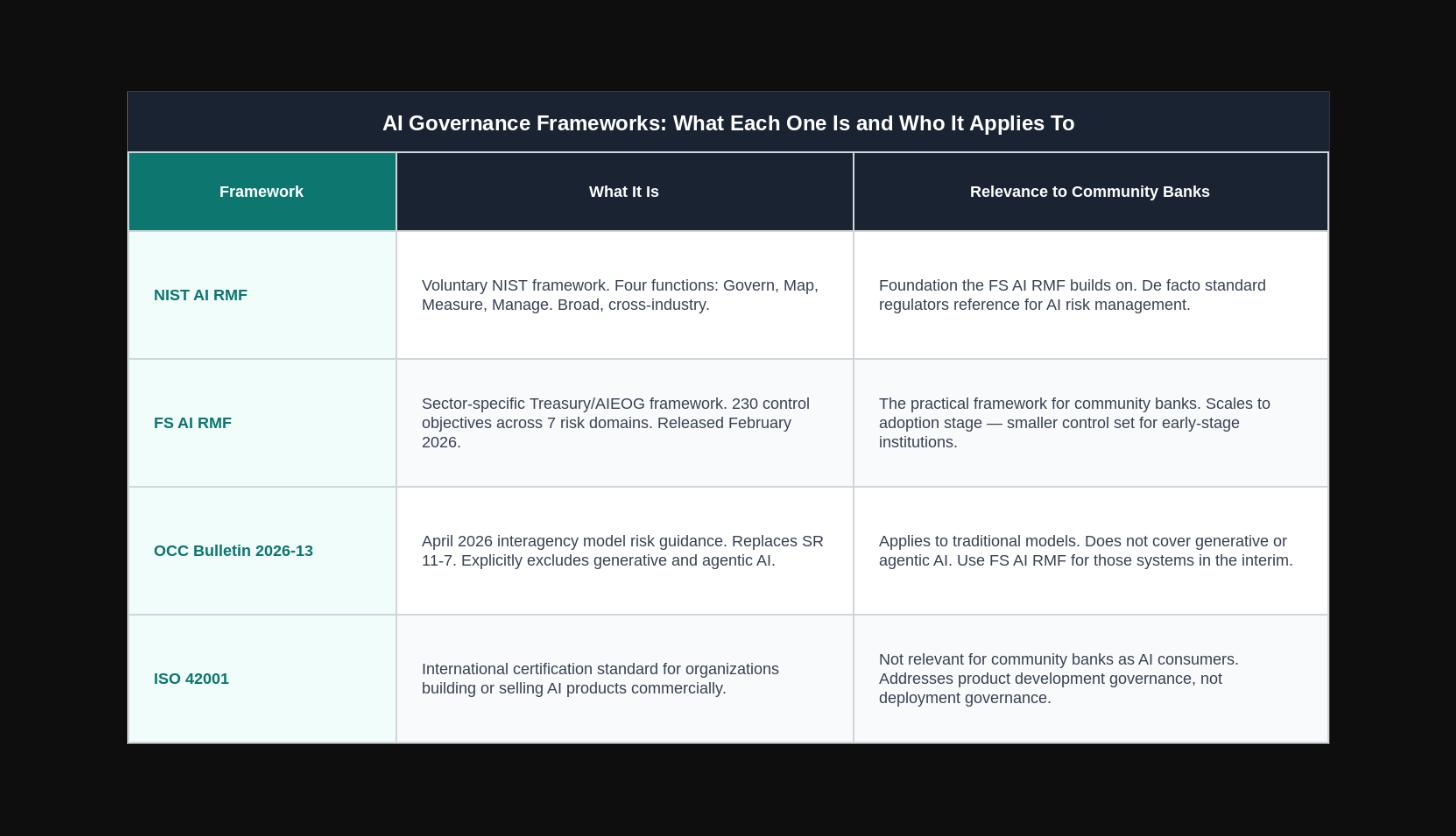

The Lexicon was published alongside the Financial Services AI Risk Management Framework (FS AI RMF), which translates the NIST AI Risk Management Framework into 230 control objectives specific to financial institutions. Both documents are available through the FSSCC AIEOG deliverables page and are described in the Treasury press release.

What the AIEOG Is and Why It Published This

The AIEOG (Artificial Intelligence Executive Oversight Group) is a public-private partnership formed by Treasury's Financial and Banking Information Infrastructure Committee (FBIIC) and the Financial Services Sector Coordinating Council (FSSCC). Its purpose is to develop practical tools for responsible AI adoption across the financial sector, not abstract policy positions.

The Lexicon is the first of six planned AIEOG deliverables addressing AI in financial services. The others cover identity, fraud, explainability, and data practices. The entire series reflects Treasury's emphasis on concrete, usable resources rather than aspirational guidance.

For community banks, the significance is straightforward. This is the language your examiners are being trained on. These are the definitions your third-party AI vendors are expected to use when they document their systems for your vendor oversight program. Understanding the vocabulary is not a compliance exercise. It is operational preparation.

Section 1: Foundational AI Terms

These are the building-block definitions. They appear in regulatory guidance, vendor contracts, and examination materials and are worth having a precise understanding of rather than an approximate one.

Artificial Intelligence (AI)

A machine-based system that can, for a given set of human-defined objectives, make predictions, recommendations or decisions influencing real or virtual environments. AI systems use machine and human-based inputs to perceive real and virtual environments, abstract such perceptions into models through analysis in an automated manner, and use model inference to formulate options for information or action.

Why it matters: The official definition is broader than most people assume. A rules-based credit scoring model counts. So does a natural language processing tool for loan document extraction. Any system using dynamic or static machine learning techniques meets this definition for governance purposes.

AI Model

A component of an information system that implements AI technology and uses computational, statistical, or machine-learning techniques to produce outputs from a given set of inputs.

Why it matters: This is the unit of analysis for model risk management. Your CECL model, your fraud detection algorithm, your transaction monitoring system, and any vendor-embedded scoring component each constitute a model under this definition and should appear in your model inventory.

Traditional AI

Traditional AI, also referred to as symbolic or rule-based AI, is a subset of AI that focuses on performing discrete, preset tasks using predetermined algorithms and rules. These AI applications are designed to excel in a single activity or a restricted set of tasks.

Why it matters: Most community bank AI today is traditional AI, deterministic systems that apply defined rules to structured inputs. Credit scorecards, rule-based fraud flags, and automated reconciliation logic fall here. The governance standards for traditional AI are more settled than for generative and agentic AI.

Generative AI

The class of AI that emulates the structure and characteristics of input data in order to generate derived synthetic content. This can include images, videos, audio, text, and other digital content.

Why it matters: Generative AI in community banking most commonly appears in customer-facing chatbots, document summarization tools, and policy Q&A applications. The AIEOG Lexicon and the April 2026 model risk guidance both flag generative AI as requiring specific governance attention beyond traditional model risk management.

Agentic AI

A category of AI systems capable of independently making decisions, interacting with their environment, and optimizing processes without direct human intervention.

Why it matters: This is the most governance-significant term in the Lexicon for community banks right now. Agentic AI takes actions, not just outputs. Systems that automatically route files, initiate notifications, update records, or move data between systems may be operating agentically even if they are not labeled as AI. For a full treatment of what this means for community banks, see the post on agentic AI in banking.

AI Agent

A system that autonomously perceives its environment, decides what to do, and takes actions to achieve its goals.

Why it matters: The distinction between an AI agent and an agentic AI system is subtle: a single AI agent is a component, while agentic AI describes a category of systems. Both share the governance concern that actions can occur without human review between each step.

Large Language Model (LLM)

A subset of machine learning that uses algorithms trained on large amounts of data through self-supervised machine learning to recognize patterns and respond to user requests in natural language.

Why it matters: LLMs underlie most of the generative AI products entering community banking through vendor channels. When a vendor describes their product as “AI-powered,” an LLM is usually what is doing the work. Understanding what an LLM does and what it cannot reliably do (see: Hallucination) is relevant for vendor due diligence.

Section 2: Risk and Governance Terms

These are the terms most likely to appear in examination conversations, vendor contracts, and internal governance discussions. Having precise definitions matters here because ambiguous language in governance documents creates audit exposure.

AI Governance

The set of organizational policies, rules, frameworks, roles, and oversight processes that direct how AI is adopted, developed, deployed, and monitored within the organization, with the objective of ensuring AI-related risks are identified, managed, and monitored across the AI lifecycle.

Why it matters: AI governance is not a document. It is an operating structure. A governance policy that is not reflected in how AI systems are actually reviewed, approved, and monitored does not satisfy this definition. Examiners asking about AI governance will look for evidence that the structure described in policy is functioning in practice.

Model Risk

The potential for adverse consequences from decisions based on incorrect or misused model outputs and reports. Model risk can be from individual models and be in the aggregate.

Why it matters: The key addition in the current environment is aggregate model risk: the interaction effects between multiple AI systems that share assumptions, data, or methodologies. Community banks with multiple vendor AI products should assess whether those products share common dependencies.

AI Risk Assessment

A risk-management process for identifying, estimating, and prioritizing risks arising from the operation and use of an AI system, incorporating threat and vulnerability analyses and considering mitigations provided by controls planned or in place.

Why it matters: An AI risk assessment is distinct from a traditional model validation. It addresses the full risk surface of an AI system, including data quality, adversarial risk, bias, and third-party dependencies — not just whether the model performs as specified.

AI Lifecycle

The set of phases an AI system goes through: plan and design, collect and process data, build and use model, verify and validate, deploy and use, and operate and monitor. These phases are often iterative, and not necessarily sequential.

Why it matters: The lifecycle framing matters for governance because oversight responsibilities change across phases. Governance documentation should address each phase rather than treating an AI system as a static product once deployed.

AI Use Case Inventory

A maintained repository or listing of an organization's AI use cases, intended to support governance, transparency, and risk management by documenting where and how AI is designed, developed, procured, or used.

Why it matters: The AI use case inventory is the governance artifact most commonly requested in early examiner conversations about AI. Banks that have a current, complete inventory are able to answer examiner questions directly. Banks without one are attempting to reconstruct it under examination pressure.

Third-Party AI Risk

Risk that arises when an organization relies on another entity to develop, provide, host, operate, or support AI systems or key AI components such as models, data, and related infrastructure.

Why it matters: Most bank AI is acquired through third-party vendors, not built internally. Third-party AI risk means the bank's vendor oversight program needs to be extended to cover AI-specific questions: what models does this vendor use, how are they validated, and what happens when the vendor updates the model without explicit notification.

Service Provider Concentration Risk

The potential for disruption or degradation at a service provider(s) to threaten the ability of a financial institution to continue performing critical activities, or cause the institution to suffer significant adverse effects.

Why it matters: Community banks with significant reliance on a single AI vendor for critical functions should document that dependency and assess the contingency plan. The Lexicon defines this at both the institution level and the financial sector level, reflecting systemic risk if many banks rely on the same vendor.

Human-in-the-Loop (HITL)

A risk-control approach for AI where a human is integrated within the AI's decision-making process.

Why it matters: HITL is not defined by whether a human can theoretically intervene in an AI process. It is defined by whether human review is actually integrated and documented within the workflow. A system that routes exceptions to a human queue with no defined review standard or logging does not fully satisfy HITL requirements in a governance context.

Explainability

Property of an AI system that enables a given human audience to comprehend the reasons for the system's behavior; the ability to understand an AI system's output and decision given certain inputs.

Why it matters: Explainability is a regulatory expectation, not just a technical property. When a regulator asks why an AI system made a particular credit decision or flagged a particular transaction, the institution needs to be able to provide a comprehensible explanation.

Black Box

The nature of some AI techniques whereby the inferential operations are complex, hidden, or otherwise opaque to their developers and end users in terms of providing an understanding of how classifications, recommendations, or actions are generated.

Why it matters: Black box AI in consumer-facing decisions creates fair lending and UDAAP exposure because the institution may not be able to explain adverse actions in terms that satisfy Regulation B.

Hallucination

A phenomenon when AI produces output that is erroneous or flawed but is still in the form of a convincing narrative or presentation. Generative AI can still produce flawed information even if underlying data is free of defects.

Why it matters: Hallucination is the reason generative AI tools should not be used in any workflow where the output is not reviewed by a human with the knowledge to identify errors. A generative AI tool that produces a confident-sounding but incorrect summary of a regulatory requirement creates liability regardless of how sophisticated the underlying model is.

Section 3: Data and Model Performance Terms

These terms describe how AI systems are built, trained, and evaluated. They are increasingly appearing in vendor documentation and examination materials.

Training Data

A subset of input data samples used to train a machine learning model.

Why it matters: Training data quality determines model quality. A fraud detection model trained on historical data that does not reflect current fraud patterns will produce outputs that reflect past conditions, not present ones. Vendor AI risk management should include questions about training data currency and representativeness.

AI Drift/Decay

The tendency for an AI model's performance to degrade over time when deployed in a real-world setting with differing conditions from those present in training and testing.

Why it matters: AI drift is why ongoing performance monitoring is a governance requirement. A model validated at deployment may perform materially differently six or twelve months later if the data environment has changed. This is particularly relevant for fraud detection and credit models.

Bias

A systematic distortion, as opposed to random error, that reduces the representativeness or accuracy of an AI system's outputs or performance for its intended purposes and operating conditions.

Why it matters: Bias in lending AI creates fair lending exposure even when the bias is unintentional. Validation documentation for any AI system used in credit, pricing, or customer segmentation decisions should address how statistical, systemic, and human bias sources were evaluated and mitigated.

Data Lineage

The history of processing of a data element, which may include point-to-point data flows and the data actions performed upon the data element.

Why it matters: Data lineage in an AI context means being able to trace any input to any model output back through the transformations and sources that produced it. Banks that cannot trace their model inputs cannot fully defend their model outputs to regulators.

Data Quality/Validity

The usefulness, accuracy, and correctness of data for its application.

Why it matters: Data quality in AI governance is distinct from general data management. An AI model may be technically well-built but produce unreliable outputs if the data feeding it is stale, incomplete, or not representative of the population it is being applied to.

Output Validation

Systematic process of verifying and confirming that AI system outputs meet specified requirements, accuracy standards, and quality criteria before being used for downstream processes.

Why it matters: Output validation prevents AI errors from propagating downstream into decisions, filings, or customer communications. It operates at runtime on actual outputs, not on the model in isolation.

Performance Monitoring

Ongoing activities that confirm an AI system is implemented appropriately, used as intended, and continues to perform as intended over time.

Why it matters: Performance monitoring is the post-deployment governance obligation most community banks have not yet systematically addressed. Acquiring and validating a model at deployment is not sufficient. The bank needs ongoing processes that would detect drift, accuracy degradation, or unexpected behavior changes.

Section 4: Adversarial and Security Terms

These terms describe threats to AI systems. They are becoming relevant for community banks through vendor risk and cybersecurity examinations.

Adversarial AI

Techniques and attacks used to manipulate AI systems, causing them to make incorrect or unintended predictions or decisions. These techniques exploit vulnerabilities in AI models, often by subtly altering input data, training data, or model interactions.

Why it matters: Primarily a vendor risk consideration for community banks. The institution's obligation is to ask vendors what adversarial testing they have conducted and what controls exist to detect adversarial inputs in production.

Data Poisoning

An attack that corrupts and contaminates training data to compromise an AI system's performance.

Why it matters: Data poisoning risk is highest for AI systems that continue to learn from operational data after initial training. If a vendor's model updates based on feedback from real-world use, the bank should understand whether the feedback mechanism can be manipulated.

Prompt Injection

An attack on an AI system that exploits how an application combines untrusted input with a prompt written by a higher-trust party, so the system follows the untrusted instructions.

Why it matters: The primary security concern for generative AI systems that process customer-submitted text. A customer service chatbot that processes free-form text from account holders is potentially vulnerable if the underlying system does not have appropriate input sanitization controls.

Deepfake

AI-generated or manipulated image, audio or video content that resembles existing persons, objects, places or other entities or events and would falsely appear to a person to be authentic or truthful.

Why it matters: In banking, deepfake risk is primarily a fraud concern: synthetic identity verification documents, AI-generated voice calls impersonating customers, and fabricated video identification. KYC processes that accept video or document-based verification without liveness detection are increasingly exposed.

Synthetic Identity

The use of a combination of real and fake personally identifiable information (PII) to fabricate a person or entity.

Why it matters: Synthetic identity fraud is among the fastest-growing fraud categories in community banking. AI-generated synthetic identities can pass traditional identity verification controls because they include real data elements. Detection requires behavioral analysis that standard onboarding processes often do not provide.

Section 5: The FS AI RMF and NIST AI RMF: What They Are and Why They Matter

The AI Lexicon was released alongside the Financial Services AI Risk Management Framework (FS AI RMF), developed by the AIEOG through the Cyber Risk Institute in collaboration with more than 100 financial institutions. Understanding the relationship between the FS AI RMF, the underlying NIST AI RMF, and existing model risk guidance is where most community banks currently have the most confusion.

What the FS AI RMF adoption stage model means for community banks

One of the most practically useful aspects of the FS AI RMF is its AI Adoption Stage Questionnaire. Rather than imposing the same 230 control objectives on every institution regardless of AI maturity, the framework defines four adoption stages and scales the control requirements accordingly. A community bank at Stage 1 (initial, using basic rule-based AI) applies a materially smaller control set than a bank at Stage 3 or 4 (AI embedded across operations and decision-making).

The first step for any community bank engaging with the FS AI RMF is to complete the Adoption Stage assessment honestly. Most community banks will find they are at Stage 1 or Stage 2, which means the required control set is manageable rather than overwhelming. The assessment is available through the Cyber Risk Institute and does not require any engagement with a vendor to complete.

The gap the FS AI RMF fills

The existing model risk framework (SR 11-7, now superseded by OCC Bulletin 2026-13) was designed for predictive statistical models: logistic regression, scorecard approaches, structured inputs, and interpretable outputs. It was not designed for large language models, document intelligence systems, or agentic workflows.

The FS AI RMF closes that gap with control objectives specifically designed for AI systems that make probabilistic outputs, learn from operational data, process unstructured content, and take automated actions. For community banks that have deployed vendor AI in any of these categories, the FS AI RMF is the most current and specific governance guidance available.

What This Means for Community Banks Right Now

The Lexicon and the FS AI RMF together establish the vocabulary and the framework that the AI governance conversation in financial services is converging on. For community banks, the practical implications are manageable and worth addressing before they become examination-driven.

Build or update your AI use case inventory. Document every AI system in operation, including those embedded in vendor products. The inventory does not have to be complex, but it has to be current and accessible.

Complete the FS AI RMF Adoption Stage assessment. This takes the framework from abstract to actionable. It identifies which control objectives apply at your institution's AI maturity level and gives you a prioritized list of governance gaps to address.

Review vendor AI documentation using the Lexicon's vocabulary. Ask vendors what models they use, how they are validated, whether they contain generative or agentic components, and what they do when those models are updated.

Assign ownership. AI governance requires named individuals responsible for the use case inventory, the ongoing monitoring program, and vendor AI oversight. Documentation without ownership does not function.

All term definitions in this post are drawn from the AIEOG AI Lexicon (February 2026), published by the U.S. Department of the Treasury, FBIIC, and FSSCC. The Lexicon is an optional tool and is not intended for use in legal interpretation of any regulations. This post is provided for educational purposes only.

Build Your AI Governance Foundation Before the Examiner Asks

Shore's free CORE Assessment evaluates operational readiness across five categories including regulatory compliance and data readiness. For community banks working through AI governance preparedness, it identifies where documentation gaps are concentrated and provides a structured starting point. The CORE Assessment takes about 20 minutes, and identifies exactly where your documentation gaps are across data readiness, regulatory compliance, and operational readiness. Build your AI governance foundation before the examiner asks.