Bank Modernization Readiness: A Practical Guide for Community Financial Institutions

Most community banks know they need to modernize. Few know where they actually stand. This guide closes the gap between wanting to change and knowing how to begin.

Table of Contents

The Gap Between "Modernize" and Knowing Where to Start

A Framework for Measuring Readiness

Data Readiness: The Foundation Everything Else Depends On

Process & Workflow: The Hidden Cost of Manual Operations

Technology & Infrastructure: When Systems Become the Bottleneck

Organizational Readiness: The Human Side of Transformation

Regulatory & Compliance Readiness: Technology Governance Under Scrutiny

What Peer Data Tells Us About Where Community Banks Actually Stand

Turning a Readiness Assessment into a Remediation Roadmap

How to Find Out Where Your Institution Stands

The Gap Between "Modernize" and Knowing Where to Start

Every community banking conference for the last five years has delivered essentially the same message:

adopt technology, modernize operations, or risk irrelevance. The OCC made it official in May 2025, issuing a formal Request for Information on community bank digitalization - a signal that regulators are no longer treating this as an aspirational topic.1 The message is clear. The path forward is not.

The 2024 CSBS Annual Survey of Community Banks, which draws responses from bankers across 38 states, found that technology implementation and costs ranked as the second-highest internal risk facing community banks - up from a tie for third the prior year.2 In the same survey, 45.6% of respondents identified "cost or ability to implement" as the single most significant impediment to adopting new technologies.3 Nearly half of community bankers aren't struggling to decide whether to modernize - they're struggling to figure out how to begin.

Meanwhile, a BNY Voice of Community Banks survey found that over 90% of community banks said they were prepared to initiate digital transformation - but fewer than 20% considered themselves experts in data analytics, the foundational capability on which most transformation initiatives depend.4 There is a significant gap between readiness as a stated intention and readiness as an operational reality.

This guide is designed to close that gap. It offers a structured framework - grounded in regulatory guidance, industry research, and operational observation - for understanding where a community financial institution actually stands across the five domains that determine modernization success. It is not a technology roadmap. It is not a vendor pitch. It is an honest assessment of what readiness looks like, what common failure patterns are, and what practical progress looks like at community bank scale.

"Modernize" is a direction. Readiness is a position. You need to know where you're standing before you can know which way to walk.

A Framework for Measuring Operational Readiness

Operational readiness is not binary. It exists on a spectrum, and most institutions are more ready in some areas than others.

The framework used throughout this guide organizes operational readiness across five distinct domains, each of which contributes to an institution's overall capacity to adopt and sustain technology-driven change:

Data Readiness - the quality, accessibility, and governance of your data assets

Process & Workflow - the efficiency, documentation, and automation potential of your operations

Technology & Infrastructure - the connectivity, flexibility, and strategic alignment of your systems

Organizational Readiness - the people, culture, and capacity needed to sustain change

Regulatory & Compliance Readiness - the governance frameworks, documentation, and audit posture your institution can demonstrate

Within each domain, readiness maps to one of five maturity levels:

These bands describe operational leverage - how well the institution's infrastructure supports its next move - not judgments about overall quality. A community bank can be financially strong, well-capitalized, and deeply committed to its community while operating in the Developing range across data or technology.

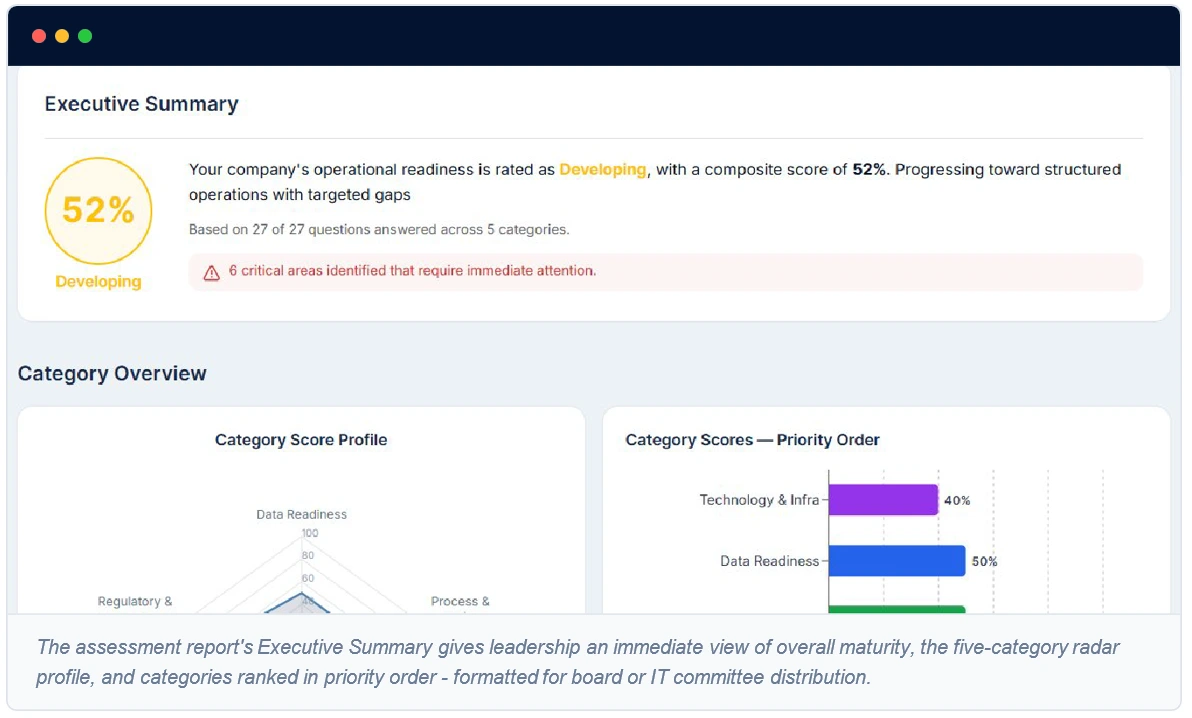

CORE benchmark context: Based on assessments completed across community financial institutions, the average overall score falls in the Developing range (41-60%). Regulatory & Compliance consistently scores highest. Data Readiness and Technology & Infrastructure consistently score lowest.

Data Readiness: The Foundation Everything Else Depends On

How well does your data support your institution's current operations - and can it support what comes next?

Data readiness is the prerequisite for virtually every modernization initiative a community bank might undertake. Before automation can eliminate manual steps, you need to know what data feeds those steps and where it comes from. Before AI can be evaluated, you need to know what your data looks like and whether it is consistent enough to rely on. Before a core conversion can be planned, you need an inventory of your data assets.

What Regulators Expect

The OCC's Interagency Guidelines Establishing Safety and Soundness include explicit standards around internal controls and information systems - and in recent examination cycles, examiners have increasingly focused on whether banks can demonstrate control over their data, not just their systems. Data governance - the documented ownership, lineage, and quality management of key data elements - has moved from a best practice to an examination expectation.

The FFIEC's guidance on data management emphasizes the need for financial institutions to maintain data integrity across systems and to demonstrate that critical data elements can be traced from source to use. When asked whether they could trace a specific data element - such as a borrower's risk rating - from its origin through every system it touches, a substantial portion of banks report they would have to "start from scratch."

Common Failure Patterns

Tribal knowledge as infrastructure. In many community banks, the institutional knowledge of how data moves between systems lives entirely in the heads of a few long-tenured employees. No formal data flow documentation exists. No data dictionary has been created. When those employees retire or leave, the knowledge goes with them - creating key-person risk that is difficult to quantify but easy to experience when something breaks.

The multi-system reporting problem. When data for a single report lives across six to eight different systems - core, LOS, CRM, compliance platform, and spreadsheet workarounds - reconciliation becomes a recurring manual project. Each cycle carries error risk, consumes FTE hours, and delays the speed at which leadership can respond to questions.

Shelfware driven by dirty data. Banks invest in analytics platforms, loan origination systems, and CRM tools - and discover after the fact that their data is too fragmented or inconsistent to make the tool work as promised.

The shelfware signal: When a bank reports that a recently purchased technology tool is "underutilized" because the data feeding it isn't ready, this is among the highest-urgency operational signals available. Addressing the underlying data issue (before purchasing the next tool) is the most important near-term priority.

DATA READINESS: SELF-ASSESSMENT QUESTIONS

Can your team produce a complete list of every system that contributes data to a regulatory report or board package?

Is there a documented, named owner for each of your institution's five most critical data elements?

Could a new employee trace a loan from origination through every system it touches without asking a colleague?

Have you invested in a technology tool in the last two years that is underperforming because the data feeding it isn't ready?

Can your institution answer an ad hoc question from a regulator within 24 hours without a multi-day data assembly project?

Process & Workflow: The Hidden Cost of Manual Operations

Where are your people doing work that shouldn't require banking judgment?

The operational burden of manual processes in community banking is substantial, largely invisible in financial statements, and widely underestimated. Manual process inefficiency doesn't generate a specific loss event - it generates a slow, persistent drain on FTE capacity, error rates, and organizational speed.

"If we added it up, it's probably 20+ hours across the team every week" - spent reformatting, re-entering, and reconciling data between systems.

- COMMON RESPONSE PATTERN ACROSS COMMUNITY BANK ASSESSMENTS

Among community banks assessed through the CORE platform, the most common gap in Process & Workflow is the proportion of work that is rule-based and repetitive but still performed manually. The most frequent answer when asked: more than 70% is rule-based - work their people do "because we don't have a better way."

The Key-Person Risk Hiding in Your Operations

The same scenario emerges repeatedly in community bank conversations: the bank's most critical operational processes are not documented in any form that a new employee could follow. The knowledge lives in the heads of experienced staff. This is sometimes called the "Brenda Factor" - the operational reality that only Brenda knows how to run the month-end reconciliation, and if Brenda is out sick on the wrong day, the process stops. The CSBS 2024 survey found that staff retention ranked as one of the top three internal risks for community banks.

The Staffing-as-a-Bandage Pattern

Adding staff or overtime to keep up with volume growth, rather than addressing the underlying workflow, is rational in the short term but creates compounding costs over time. The loan boarding process is a useful illustration: for many community banks, onboarding a new commercial loan takes several weeks because it involves document gathering, manual data entry across multiple systems, cross-department handoffs, and ad hoc exception handling at every step.

PROCESS & WORKFLOW: SELF-ASSESSMENT QUESTIONS

Could a new employee follow your five most critical back-office processes using only written documentation?

How many hours per week does your team spend re-entering the same data into multiple systems?

Have you added staff or overtime in the last two years to handle volume growth in any operational area?

Do you have a quantified understanding of the cost - in FTE hours, error rates, and cycle time - of your most resource-intensive processes?

In your most time-consuming recurring task, how many people or departments does it touch before completion?

Technology & Infrastructure: When Systems Become the Bottleneck

Are your existing systems enabling modernization - or making it harder?

The core banking system is simultaneously the institution's most critical operational infrastructure and, in many cases, the primary constraint on its ability to innovate. The CSBS 2023 Annual Survey found that 64% of community banks cited core processor responsiveness as a significant challenge to implementing new technology.6 When your core provider controls data access, integration timelines, and the vendor ecosystem, your technology strategy is partially determined by decisions made outside your institution.

The Data Sovereignty Question

Can we access, extract, and move our own data when we need to? For banks that depend heavily on their core provider for data access - where even routine extracts require a support ticket and a wait - the answer reveals a form of vendor dependency with significant strategic implications. When a bank cannot access its own data independently, it cannot easily evaluate new technology tools, build analytical capabilities, or move quickly in response to examiner requests.

Integration Friction and Innovation Paralysis

One of the most common Technology & Infrastructure findings is a history of technology initiatives delayed or abandoned because of integration challenges. A meaningful number of institutions report they have largely stopped trying to bring in new tools because of how painful the integration process has become. Innovation paralysis is a real phenomenon - its root cause is typically not a lack of appetite for technology but a lack of integration infrastructure to support it cost-effectively.

The Spreadsheet Dependency Signal

The risk emerges when spreadsheets become critical operational infrastructure: the file that runs the reconciliation, the workbook that generates the regulatory report, the model that prices loan exceptions. When spreadsheets serve these functions, they create version control risk, key-person risk, audit risk, and data integrity risk at every step. The OCC's guidance on model risk management applies to spreadsheet-based models used for critical functions.

TECHNOLOGY & INFRASTRUCTURE: SELF-ASSESSMENT QUESTIONS

Can your institution access and extract any data element from your core system without involving your core vendor?

How many of your current software vendors offer API access versus requiring batch file transfers or manual data pulls?

Has your institution experienced a technology initiative delayed or abandoned due to integration challenges?

Are spreadsheets serving as critical operational infrastructure for any regulatory, compliance, or reporting function?

Does your institution have a documented technology roadmap that extends beyond the current fiscal year?

Organizational Readiness: The Human Side of Transformation

Does your institution have the leadership alignment, talent, and change management capacity to sustain what technology makes possible?

Technology can create the conditions for operational improvement, but it cannot create the organizational capacity to act on those conditions. The most sophisticated data infrastructure produces no value at a bank where leadership has not aligned around priorities, where operational ownership is diffuse, or where previous technology implementations left the organization reluctant to try again.

The Ownership Gap

In many community banks, the honest answer to "who owns operational efficiency?" is: "It's everyone's job and nobody's job. Improvement happens when someone gets frustrated enough to speak up." Without a champion, priorities shift with the calendar. Projects that have no dedicated owner stall when a competing priority - an exam cycle, a loan pipeline surge, a system outage - consumes the available bandwidth.

Board Engagement and Strategic Velocity

When board discussions about technology consist primarily of aspirational comments without specific metrics, progress reviews, or budget alignment, the organization receives a signal that improvement is a nice-to-have. The OCC has explicitly noted in its RFI that it seeks to understand how boards of directors oversee and support digitalization - a signal of examiner attention to board-level technology governance, not just management-level execution.

Talent Pressure and the Automation Case

Competition for skilled operations, compliance, and technology staff has intensified, and community banks are at a structural disadvantage relative to larger institutions and non-bank employers. Each manual process that depends on a specific individual is a vulnerability. Automating the rule-based portions of those processes reduces key-person risk, creates headroom for experienced staff to focus on judgment-intensive work, and makes remaining roles more sustainable.

ORGANIZATIONAL READINESS: SELF-ASSESSMENT QUESTIONS

Is there a named individual in your institution with genuine accountability for operational efficiency or data strategy - with dedicated budget?

When your board discusses technology, do those conversations produce specific metrics, action items, and budget alignment?

How has your institution responded to previous technology implementations - and how does that history affect appetite for the next one?

Do you have a realistic assessment of key-person risk in your operations and compliance functions?

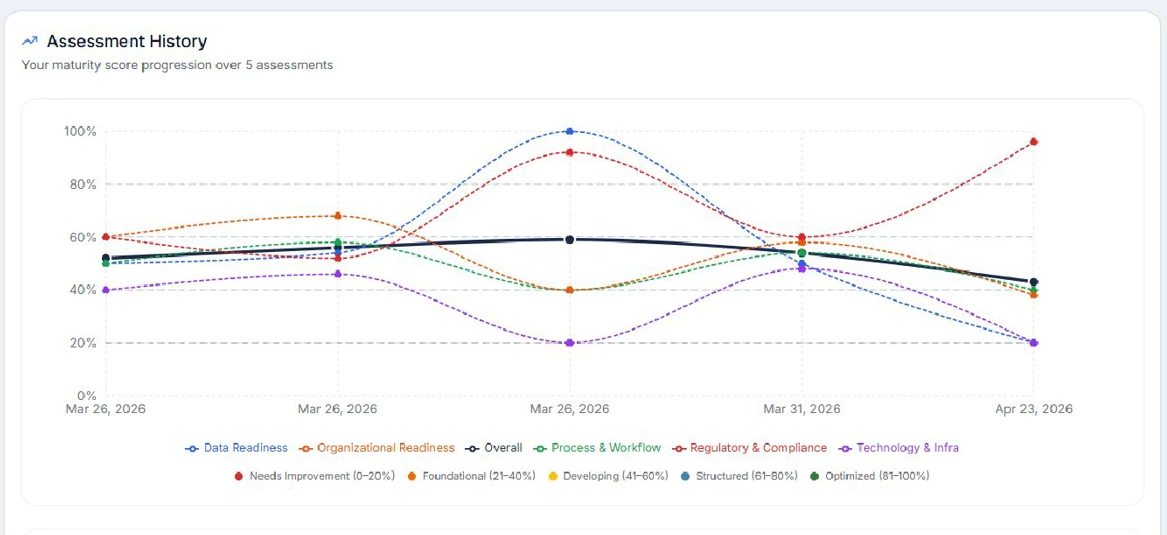

Is your institution actively benchmarking its operational performance against peers?

Regulatory & Compliance Readiness: Technology Governance Under Scrutiny

Can your institution demonstrate control, governance, and preparedness - not just in operations, but in how it adopts and manages technology?

Regulatory & Compliance Readiness is where community banks most often score highest - and with good reason. But the nature of examiner scrutiny is shifting. The traditional focus on whether a bank complies with specific rules is being supplemented by newer questions: how does the bank govern technology adoption, what controls exist around data shared with third-party vendors, and how does the institution demonstrate operational resilience?

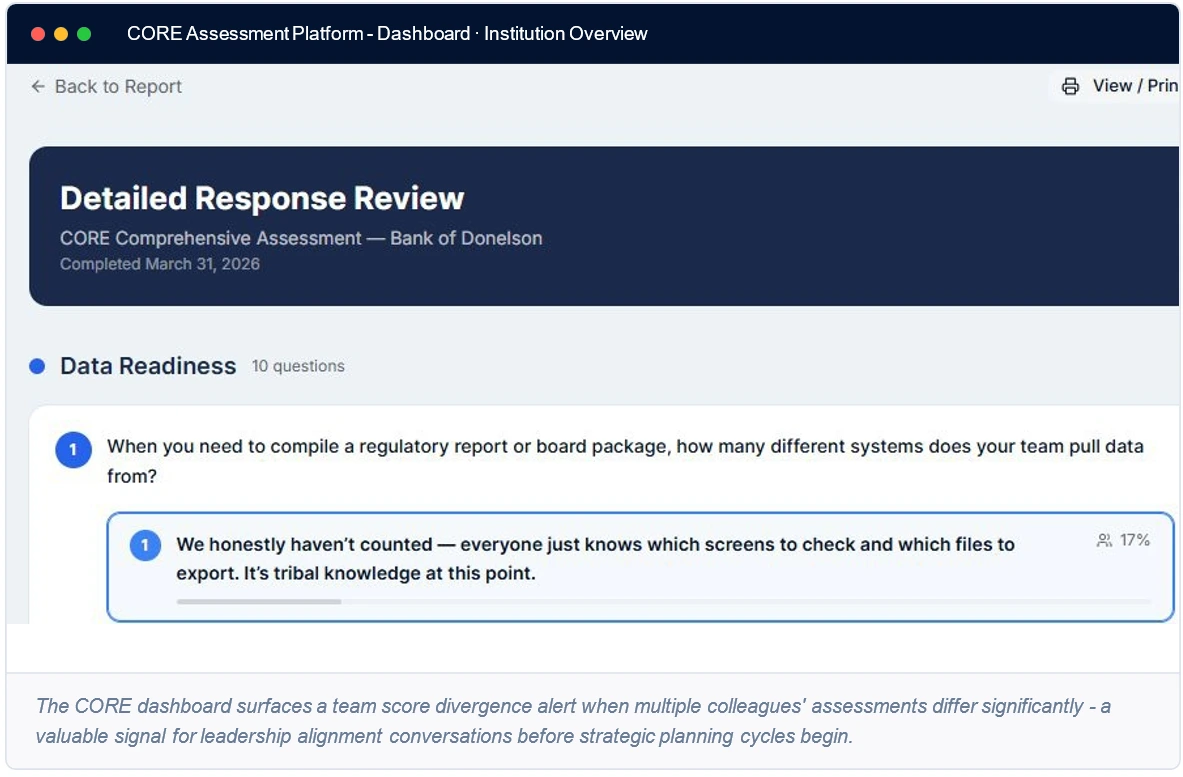

The CORE dashboard surfaces a team score divergence alert when multiple colleagues' assessments differ significantly - a valuable signal for leadership alignment conversations before strategic planning cycles begin.

Third-Party Risk Management: The 2023 Interagency Guidance

In 2023, the OCC, Federal Reserve, and FDIC issued updated interagency guidance on third-party relationships, formalizing expectations around due diligence, ongoing monitoring, and exit planning for third-party relationships. For many institutions, vendor relationships are still managed in spreadsheets, file folders, and email threads - with no centralized inventory, no documented risk tiering, and no formal process for evaluating whether data-sharing arrangements meet current expectations.

AI Governance: From Aspiration to Expectation

Regulators expect financial institutions to have a formal position on AI - not necessarily to be using it, but to have considered the risks, documented their approach, and established governance frameworks. The OCC's May 2025 RFI includes explicit questions about how banks are managing AI-related risks. Institutions that have a documented AI governance framework - even a basic one defining acceptable use cases and oversight responsibilities - are meaningfully better positioned than those still treating AI as a future consideration.

Exam Preparation: The Reactive-to-Proactive Shift

Banks that have moved toward proactive exam preparation - maintaining standing reports, pre-built data packages, and continuously updated documentation - absorb the same workload more efficiently, reduce error risk, and present to examiners with greater confidence. The technology investments that enable this shift are fundamentally data readiness and process automation investments that provide compliance benefits as one of several outcomes.

REGULATORY & COMPLIANCE READINESS: SELF-ASSESSMENT QUESTIONS

Does your institution have a centralized, current inventory of all third-party vendor relationships with documented risk tiering?

Has your institution developed a formal position on AI - including acceptable use policies and oversight responsibilities?

How much of your exam preparation is proactive versus assembled under time pressure in the weeks before examiners arrive?

Were any data, reporting, or operational control matters raised in your most recent examination - formally or informally?

Does your business continuity plan address operational process continuity, or primarily physical disaster recovery?

What Peer Data Tells Us About Where Community Banks Actually Stand

Aggregate patterns from completed assessments reveal consistent strengths, consistent gaps, and significant variation within peer groups.

One of the most valuable outputs of a structured assessment framework is the ability to compare an institution's results against peers in operational terms - which have historically had no equivalent benchmarking source to match the UBPR and call report data available for financial comparison.

Regulatory & Compliance consistently scores highest. The gap between compliance scores and scores in other domains is often significant. Banks can present well to examiners while carrying meaningful operational risk in data, process, and technology domains that are not yet subject to the same examination focus.

Data Readiness and Technology & Infrastructure consistently score lowest. A bank that scores in the Foundational range on data readiness will find that its ability to improve in every other domain is constrained - because data readiness is a prerequisite for process automation, technology integration, and compliance analytics alike.

Significant variation exists within peer groups. The score distribution is bimodal - with a cluster of institutions in the Developing range and a smaller cluster at the high end of the Structured range. Peer comparison at the asset tier or state level reveals meaningful performance gaps that aggregate sector-level data obscures.

CSBS data confirms that most community banks benchmark themselves financially against peers with regularity - but almost none benchmark their operational performance against peers with comparable rigor. When a bank sees, for the first time, that its Technology & Infrastructure score places it in the 2nd percentile relative to peer institutions, the reaction is typically not defensiveness but clarity. The gap becomes concrete and actionable in a way that a general sense of "we need to modernize" never does.

Turning a Readiness Assessment into a Remediation Roadmap

Knowing where you stand is the beginning. What comes next determines whether anything changes.

An assessment that produces a score and a report but no structured follow-through generates limited value. The purpose of understanding where an institution stands is to inform what it does next - and that requires translating findings into specific, assigned, time-bound actions.

Effective remediation follows a logical sequencing principle: address the dependencies first. Because data readiness is foundational to progress in other domains, it is almost always the right starting point - even for institutions whose most visible pain is in technology or process. A bank that automates a process built on inconsistent data will automate the errors along with the workflow.

The practical sequence for most community banks in the Developing range: establish data foundations → document and standardize critical processes → address the highest-impact integration gaps → build organizational capacity and board alignment around a multi-year roadmap.

Find Out Where Your Institution Actually Stands.

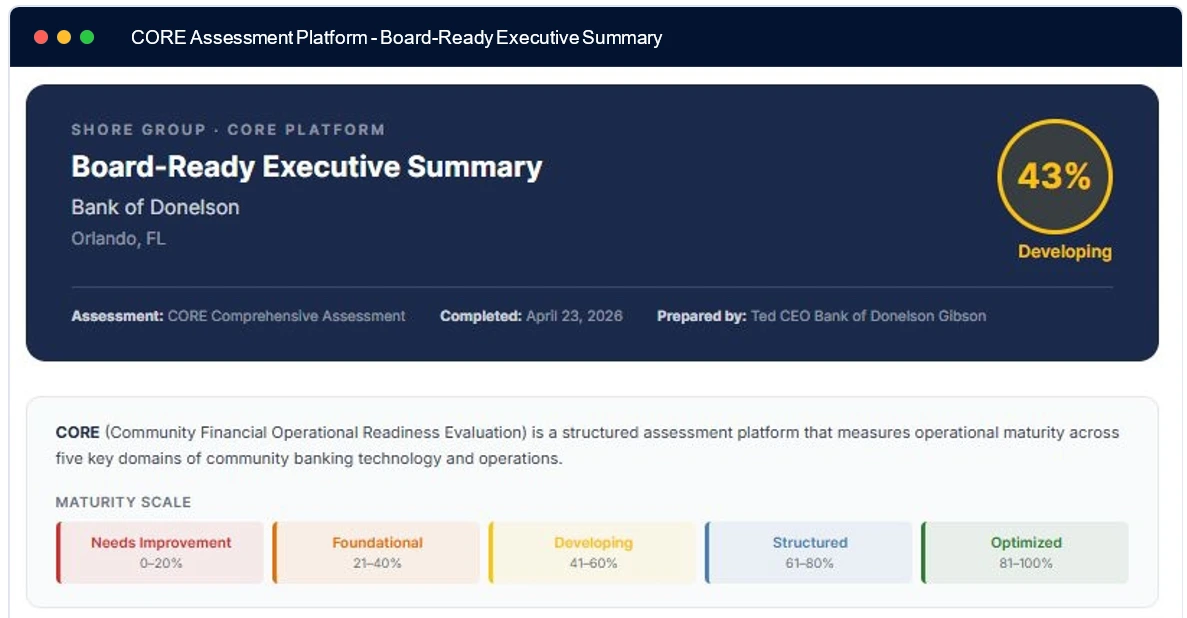

The CORE Assessment is a free, structured evaluation built specifically for community financial institutions. It takes 30-45 minutes, covers all five operational domains, and produces a scored report with peer benchmarking, category-level findings, and prioritized recommendations you can bring directly to your board.

✓ Peer benchmarking by institution type and asset tier

✓ Category-level gap analysis with specific findings

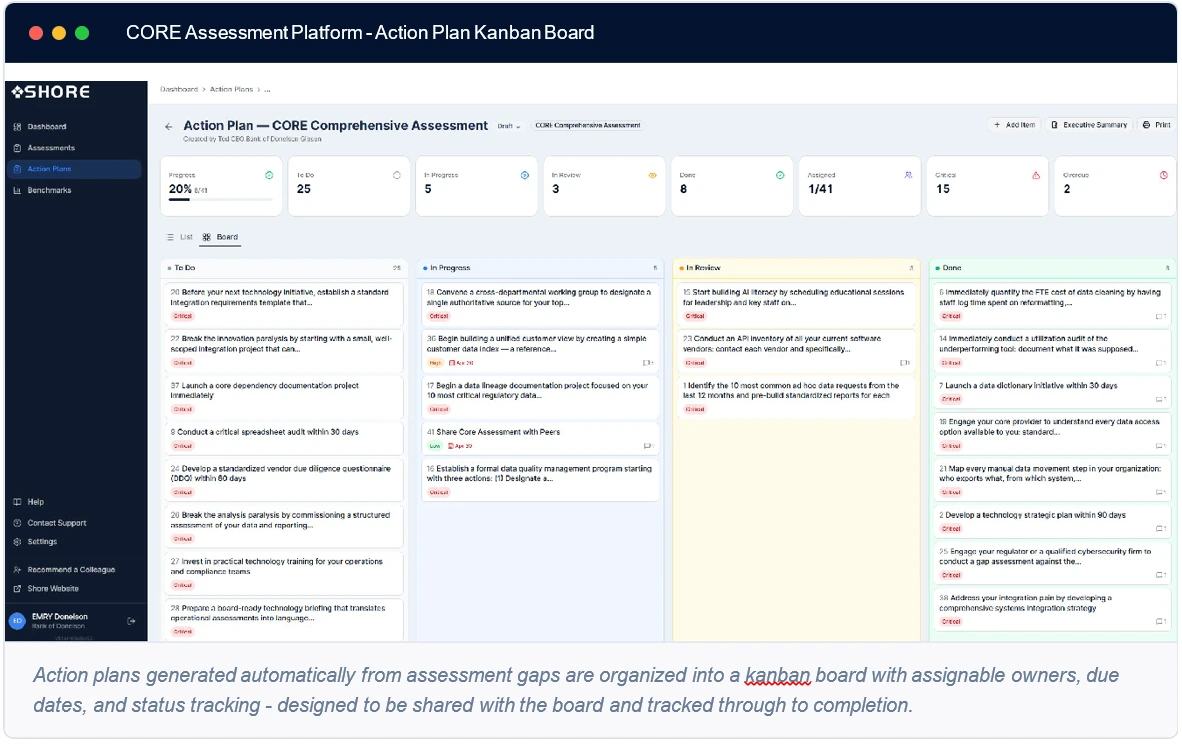

✓ Auto-generated action plan from assessment gaps

✓ Board-ready executive summary - exportable in minutes

✓ Team alignment check - compare colleague perspectives

Both assessment tiers and all outputs are completely free. No paywall, no trial period, no sales follow-up unless you request it.