BSA/AML Automation for Community Banks: Reducing Alert Volume Without Adding Staff

Most BSA/AML alerts are false positives. Here is how a three-tier routing model concentrates analyst time on the alerts that actually require judgment.

TL;DR

Most BSA/AML transaction monitoring alerts are false positives. The triage burden at community banks is high because every alert, regardless of risk level, requires data assembly before any analysis can begin. BSA/AML automation does not reduce regulatory quality. It reduces the time spent on data assembly by routing alerts with context already assembled and clearing low-risk items automatically against defined criteria. Analysts concentrate on alerts that genuinely require judgment. Documentation quality improves because every disposition is logged systematically rather than recorded manually.

Community banks operate BSA/AML programs with compliance teams that are small relative to the transaction volume they monitor. A $600M community bank processing 50,000 transactions per week can generate hundreds of alerts from its transaction monitoring system. Most of those alerts represent routine activity that will not lead to a SAR filing. But each one still requires someone to pull transaction history, review account context, check prior alert history, and document a disposition decision.

When that work falls on one or two BSA analysts, the cumulative burden is significant. Teams that are stretched thin take longer per alert, produce less thorough documentation, and have less capacity for the genuine investigations that require real analytical judgment. The volume problem and the quality problem are the same problem. BSA/AML automation addresses this by separating the data assembly work from the analytical judgment work. The former is automatable. The latter is not, and should not be.

OCC Bulletin 2025-37a, effective February 2026, established new Community Bank BSA/AML Examination Procedures that emphasize examiner discretion and allow reliance on satisfactory independent testing. The practical implication: banks with well-documented, risk-based alert management programs benefit from a more efficient examination. Banks whose alert triage is inconsistent or poorly documented face the same scrutiny as before.

The Alert Volume Problem at Community Banks

Transaction monitoring systems are configured to generate alerts when transaction activity matches defined risk patterns: amounts above certain thresholds, geographic risk indicators, transaction types associated with known money laundering typologies, and behavioral anomalies relative to a customer's historical profile.

In practice, these rule sets generate a large number of alerts, the majority of which clear on review. Industry estimates consistently place false positive rates in BSA/AML transaction monitoring at 90-95% of total alerts. The alerts are not wrong to generate. The monitoring system is doing its job by flagging potential risk indicators. The problem is that every alert, regardless of whether it will lead to anything, currently requires the same manual data assembly process before a disposition decision can be made.

At a community bank with limited BSA staff, this creates a compounding problem. High alert volume consumes analyst capacity. Constrained capacity means longer time per alert and less thorough documentation. Poorer documentation creates examination risk even when the underlying decisions were sound.

At a 95% false positive rate, a bank generating 200 alerts per week will conduct roughly 190 reviews that lead nowhere. If each alert takes 20 minutes of data assembly plus 10 minutes of analysis and documentation, that is 63 hours per week on triage before any genuine investigation begins. Reducing the data assembly time on routine alerts from 20 minutes to near zero reclaims a substantial share of that capacity for the alerts that actually matter.

Can BSA/AML Automation Solve The Problem?

The core function of BSA/AML automation is to separate two activities that currently happen in sequence: data assembly and analytical judgment. Data assembly (pulling transaction history, account context, prior alert history, and any associated documentation) is rule-based and repeatable. It is the right kind of work to automate. Analytical judgment (determining whether a pattern represents genuine suspicious activity, drafting a SAR narrative, deciding whether to escalate) requires human expertise and cannot be automated responsibly.

A well-designed automated BSA/AML workflow handles data assembly and initial risk scoring, routes items by risk tier, and routes only items that require genuine judgment to the analyst queue. The analyst opens an alert that already has everything they need to make a decision. They are not starting an investigation. They are reviewing a case file.

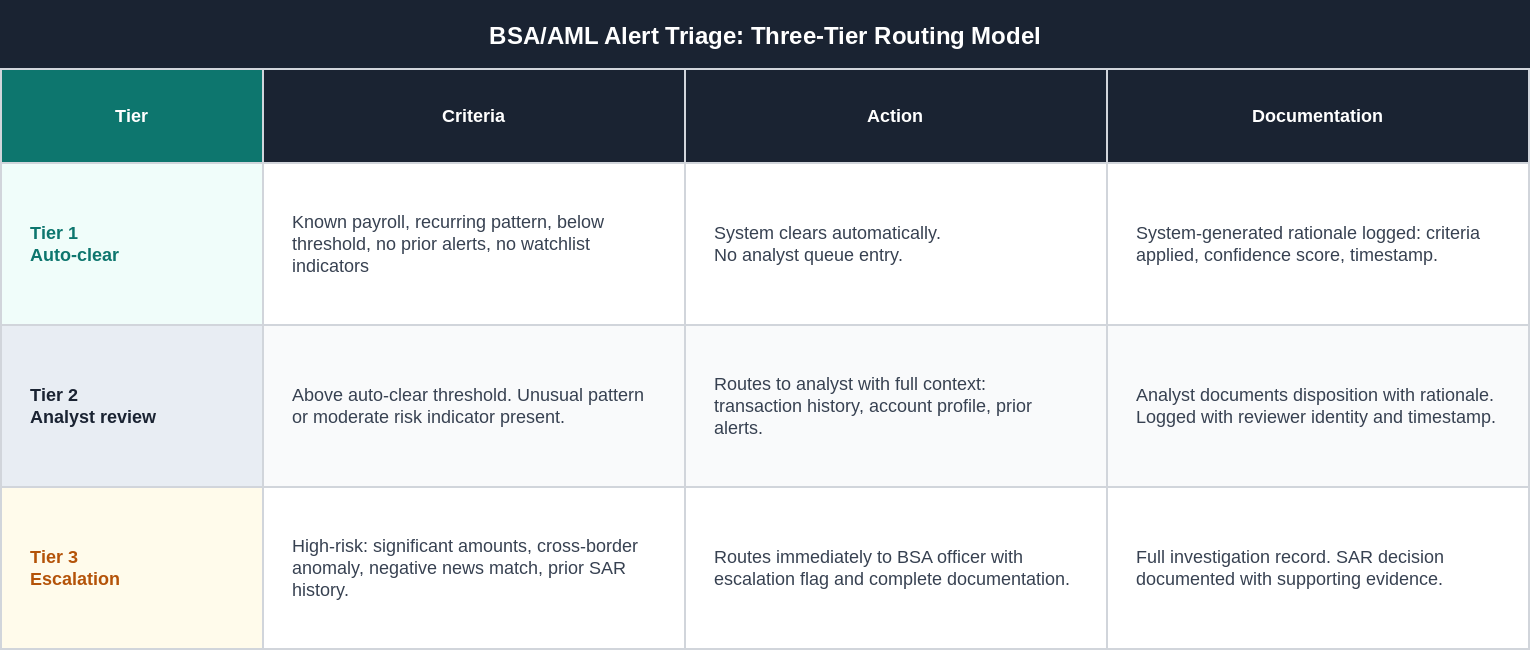

The Three-Tier Routing Model

What Changes for the Compliance Team

The most important operational change is not the reduction in alerts that reach analysts. It is the quality of the information that arrives with each alert that does.

Under a manual process, an analyst opening an alert spends most of their time gathering context before they can begin analysis: pulling statements, reviewing prior history, checking watchlists, assembling a coherent picture of the activity. The actual decision about whether the activity is suspicious takes a fraction of the total time.

Under an automated workflow, all of that context is assembled by the system before the alert reaches the queue. The analyst spends their time on the decision, not the assembly. The time per alert drops significantly. Documentation quality improves because the context is captured systematically rather than manually noted. And the analyst's capacity for genuine investigation increases because they are not spending the majority of their time on data retrieval.

The Examiner Question: Does This Satisfy BSA Requirements?

The short answer is yes, when the program is designed correctly. BSA/AML examination does not require that every alert receive manual human triage. It requires that the bank's program be risk-based, consistent, and documented. An automated program that applies defined criteria, documents every auto-clear decision with a logged rationale, and routes genuine exceptions to human review produces documentation that is more complete and consistent than most manual programs, not less.

The OCC's 2025 community bank BSA/AML examination procedures reinforce this explicitly: examiners are directed to exercise discretion and may rely on satisfactory independent testing rather than conducting transaction-by-transaction review. Banks with well-configured automated programs and current independent testing results are in a stronger examination position, not a weaker one.

What the examiner does require is transparency about the auto-clear criteria. The bank must be able to explain what criteria a Tier 1 alert meets, why those criteria represent acceptable risk, and how those criteria were determined. This is a governance and documentation question, not a technology question.

Vendor AI in Transaction Monitoring

Most community bank transaction monitoring systems include AI or statistical models built by the vendor. The alert scoring, risk indicators, and behavioral baseline models are not configured by the bank. They are embedded in the purchased product. This creates a specific governance obligation that many community banks have not fully addressed. As covered in the post on AI governance for community banks, the bank owns the governance responsibility for vendor models regardless of who built them.

In practical terms, this means the bank should have documentation of what the vendor's transaction monitoring model does, how it was validated, and how the bank has evaluated whether it is performing appropriately in the bank's specific operating environment. When the vendor updates the model, the bank should have a process for reviewing the change and documenting its assessment. This is not a burdensome requirement. It is a documentation discipline that most banks have not yet applied to their monitoring systems.

Example: A Community Bank Managing 300 Alerts Per Week

A $750M community bank generates approximately 300 transaction monitoring alerts per week. With two BSA analysts, each alert currently requires roughly 25 minutes of manual data assembly and review. That is approximately 125 analyst hours per week, before any genuine investigation or SAR work begins.

Under a three-tier automated routing model, the distribution shifts. Approximately 200 of the 300 weekly alerts meet Tier 1 auto-clear criteria and clear automatically with system-generated documentation. Approximately 80 route to Tier 2 with context assembled, each requiring 10 minutes of analyst review rather than 25. Approximately 20 route to Tier 3 as genuine escalations requiring full investigation.

The analyst time committed to triage drops from 125 hours per week to approximately 16 hours. The remaining capacity goes to investigation quality, SAR narrative development, independent testing support, and regulatory reporting. Documentation quality improves because every auto-clear disposition is logged systematically. The program becomes more defensible on examination, not less.

What BSA/AML Automation Does Not Do

Being explicit about the limits of automation matters here because BSA/AML is a regulated function with specific documentation and governance requirements.

Automation does not file SARs. SAR decisions require human judgment and are the bank's BSA officer's responsibility regardless of how the underlying alert triage is handled.

Automation does not replace the bank's BSA program. The risk assessment, policies, training program, and independent testing remain the bank's obligations. Automation handles alert management within that program, not the program itself.

Automation does not guarantee examination success. A well-designed automated program that is poorly governed, poorly documented, or not calibrated to the bank's actual risk profile will not satisfy examination expectations.

Automation does not remove the need for the human-in-the-loop model for items that genuinely require analytical judgment.

Remember: The Tier 3 escalation is not an optional component of the design. It is the mechanism that ensures genuine suspicious activity reaches an analyst who can evaluate it appropriately.

Frequently Asked Questions

Does automating alert triage satisfy FinCEN's BSA requirements?

Yes, when designed appropriately. FinCEN's BSA requirements specify that banks must have a risk-based program with procedures reasonably designed to identify suspicious activity. They do not require that every alert receive individual manual review. An automated program that applies risk-based criteria, documents every disposition, and escalates genuine concerns to human review satisfies the risk-based program standard. The key requirements are that the auto-clear criteria are defined and documented, that the bank has evaluated whether those criteria are appropriate for its risk profile, and that the program is subject to independent testing.

What criteria should define the auto-clear threshold?

Auto-clear criteria should be specific enough to be defensible and conservative enough that clearing an alert automatically does not create meaningful risk of missing genuine suspicious activity. Common auto-clear criteria include: transaction originates from a known employer identified in the customer's file, transaction amount is consistent with historical baseline and below a defined threshold, no prior alert history on the account, no watchlist indicators on any related party, and transaction type is not associated with known high-risk typologies for this customer segment. The criteria should be reviewed and approved at the appropriate governance level and documented in the bank's BSA program policy.

How does a community bank document its automated disposition logic for an examiner?

The examiner needs to be able to answer three questions about any auto-cleared alert: what criteria did the system apply, why are those criteria considered acceptable risk, and how was the auto-clear decision logged. The first question is answered by the system log, which should record which specific criteria the alert matched. The second is answered by the bank's BSA policy documentation, which should define the auto-clear criteria and the governance process by which they were established. The third is answered by the audit trail, which should show that the auto-clear event was recorded with a timestamp, the criteria applied, and a confidence indicator.

What is the difference between transaction monitoring and case management?

Transaction monitoring is the process of reviewing transaction activity against defined risk rules to identify potential suspicious activity. Case management is the process of documenting an investigation into a specific customer or set of transactions that have been identified as warranting deeper review. Transaction monitoring produces alerts. Case management handles the alerts that escalate to genuine investigation. An automated workflow sits primarily in the transaction monitoring layer, improving how alerts are triaged and routed before they reach the case management stage. The two functions are connected but distinct, and automation serves a different role in each.

Can a small community bank with limited IT resources implement BSA automation?

The level of BSA/AML automation appropriate for a given institution scales with its size, complexity, and alert volume. A $250M community bank generating 30 alerts per week has a different starting point than a $750M bank generating 300. The managed services approach addresses the IT resource constraint directly: rather than the bank configuring and maintaining automation internally, a managed service provider handles the workflow design, system configuration, and ongoing maintenance. The bank defines the auto-clear criteria and oversight requirements. The provider builds and runs the workflow. This is the appropriate model for community banks that need the operational benefit without the internal technical build.

Ready to Reduce Your Alert Burden?

Shore Group manages BSA/AML alert workflows for community banks end to end — alert triage, context assembly, risk-tiered routing, and audit trail generation — with SLA-backed accuracy and documentation ready for examiner review.

Learn How We Work