Back-Office Automation for Community Banks: No New Headcount. No New Software.

Most community banks assume automation requires a software project or new hires. A managed service delivers the result without either.

TL;DR

Most community banks assume back-office automation requires one of two things: a software implementation project or additional headcount. A managed service delivers the operational outcome without either. No implementation timeline. No hiring cycle. No new system to maintain. The provider owns the workflow and delivers a defined result. This post explains what that looks like across five specific back-office functions, and why the engagement model is lower-risk than the alternatives.

For the third consecutive year, automation and AI top the list of technology priorities for community banks. According to CSI's 2026 Industry Outlook, 37% of bankers cite automation as critical to improving back-office processes, and the pressure to do more with less is not diminishing. The challenge is not awareness of the need. It is the perceived cost and complexity of acting on it.

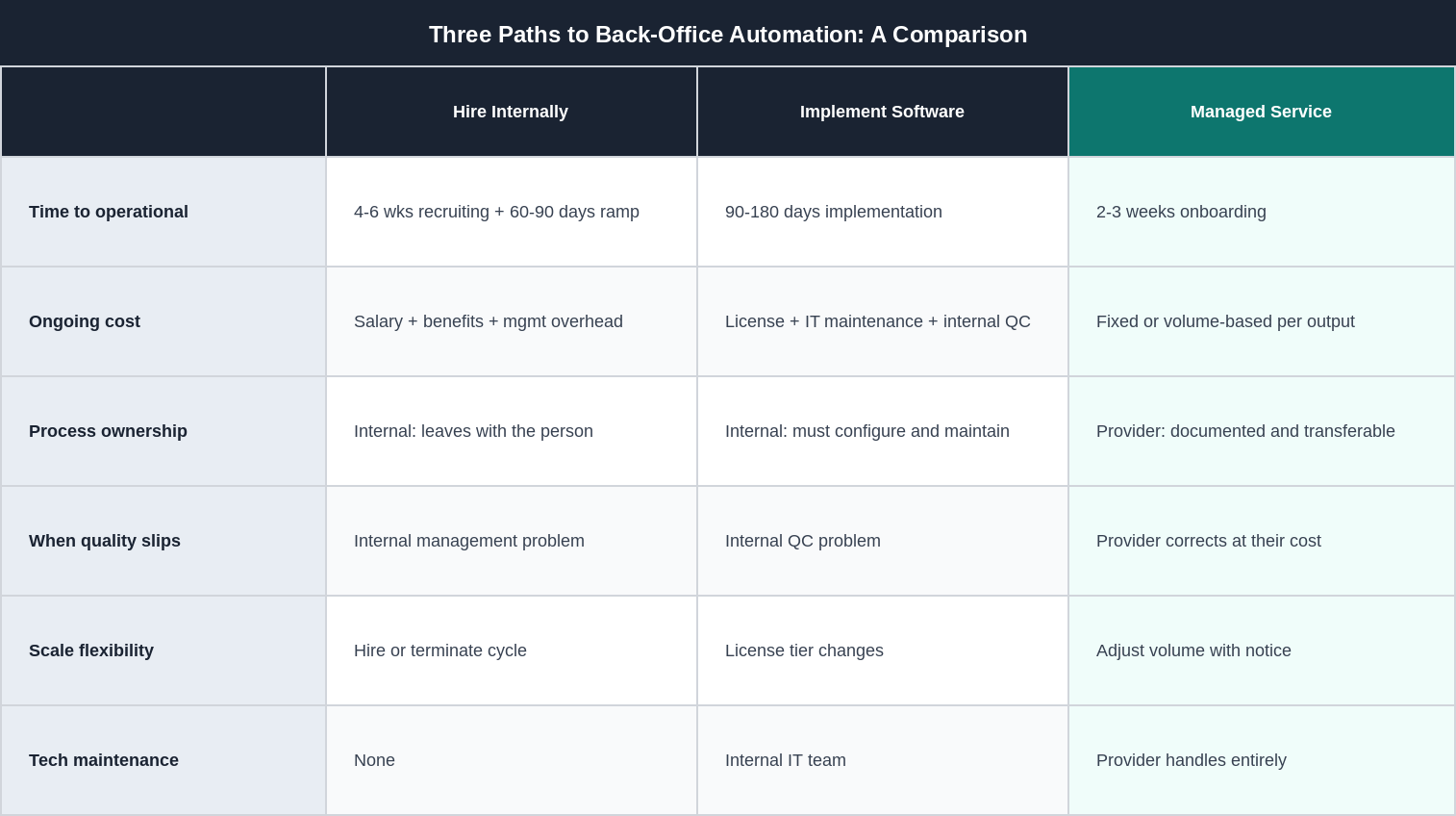

Two assumptions drive inaction. The first is that back-office automation requires a software implementation: vendor selection, contract negotiations, IT integration, user training, and months of configuration before anything actually changes. The second is that handling more volume requires more people: post a job, hire someone, onboard them, train them, and absorb the management overhead that comes with every new hire.

Both assumptions have a third option that most community banks have not fully considered: a managed service that owns the workflow end to end and delivers a defined output. No software to implement. No staff to hire. No implementation project. Just the result.

The Two Things Every COO Is Trying to Avoid

The typical framing for back-office improvement at a community bank puts two options on the table - how do I get more output out of my people or do I need to implement software to speed up my process? The problem is, both also carry costs and timelines that cause operations leaders to defer action repeatedly.

The hiring path

Bringing a new person on board to handle a back-office function takes four to six weeks to recruit, two to four weeks to onboard, and 60-90 days before the hire reaches full productivity. Total cost including salary, benefits, equipment, and management overhead typically runs 1.3-1.5 times base salary per year. And the process knowledge lives in the person, not in documented systems, which means the problem of operational continuity resurfaces every time someone leaves.

For functions that have grown faster than the team, hiring is the right answer. For functions that are primarily manual and repeatable, it is an expensive way to defer the underlying process problem.

The software implementation path

Software solves the wrong problem in most back-office automation scenarios. The tool provides the capability. The bank still has to configure it, integrate it with existing systems, train staff on it, and maintain it over time. When something breaks or when the process changes, the bank's team handles the remediation. The vendor delivered a platform. What the bank does with it is the bank's responsibility.

For functions where the bank wants to own the technology long-term and has the internal capacity to implement and maintain it, software is appropriate. For most community bank back-office functions, the bank wants the result, not the tool.

A managed service takes ownership of the workflow and delivers a defined output. The provider handles everything required to produce that output: the people, the technology, the process design, the quality assurance, and the exception handling. The bank defines what it needs and reviews the result. Implementation timeline: two to three weeks. Additional headcount on the bank's org chart: zero. Ongoing technology maintenance responsibility: zero.

What Does Managed Back-Office Automation Looks Like

The managed service model for back-office automation operates differently from both staffing and software. The provider takes responsibility for a specific workflow and commits to delivering a defined output under a service level agreement. The bank does not manage the team day to day. The bank does not configure or maintain the tools. The bank defines the requirements, reviews the output, and escalates when the standard is not met.

The workflow runs on the provider's infrastructure, using a combination of automation and human-in-the-loop quality assurance for exceptions that the automated portion cannot handle cleanly. The bank receives a data product: clean, validated output in whatever format its downstream systems require. The provider owns the accuracy of that output.

Five Workflows Community Banks Run This Way Today

These are not hypothetical applications. They are the specific workflows community banks are currently running through managed service models without software implementations or additional headcount.

1. Loan document processing

Commercial loan packages arrive via email and portals, often 50-100 pages per borrower, in mixed document formats. A managed workflow ingests each package, classifies the document types, extracts financial data across all documents, cross-validates figures between sources, and delivers LOS-ready structured output. Underwriters receive a complete, validated data package rather than a stack of PDFs to work through manually.

See the post on loan document processing for a detailed breakdown of what this looks like at a community bank.

2. Daily reconciliation

Transaction files from ACH, wire systems, card processors, and the general ledger feed into an automated matching workflow each morning. Routine matches clear without analyst involvement. Exceptions route with source documentation assembled and a suggested resolution where the data supports one. The finance team starts each day with a current exception queue rather than a blank reconciliation spreadsheet.

For a full treatment of how this works, see the post on bank reconciliation automation.

3. Compliance data aggregation

Data required for BSA/AML documentation, regulatory reporting, and exam preparation is aggregated automatically from source systems on defined schedules. Gaps, discrepancies between source systems, and values outside expected ranges surface before filing deadlines rather than during exam preparation. The compliance team receives a current, validated dataset rather than spending days assembling one manually from multiple system exports.

4. KYC document intake and verification

Onboarding documents for new commercial relationships are received, classified, and checked against required document checklists automatically. Missing items are flagged and tracked. Data fields are extracted and submitted to watchlist screens without analyst data entry. Only genuine exceptions, ambiguous matches, or complex ownership structures route to the compliance analyst for judgment.

5. Exception handling and escalation routing

Across all workflows, items that fall outside defined parameters route to the appropriate internal reviewer with context already assembled: the source document, the extracted data, the specific issue flagged, and any prior history on that item or account. The reviewer makes a decision and the resolution is logged. Nothing sits in a queue waiting for someone to remember to follow up on it.

The Three-Path Comparison

What This Engagement Actually Requires from the Bank

The managed service model requires less from the bank than either hiring or software implementation, but it requires specific things done well. Vague requirements produce inconsistent results regardless of the delivery model.

A defined scope: what workflow is being handed off, what the inputs are, what the output needs to look like, and what accuracy standard is acceptable.

A brief discovery engagement: two to four conversations in which the provider maps the current process, identifies the data sources, and defines the exception handling logic.

Approval of the delivery team: the bank reviews and approves the professionals assigned to the engagement before they begin.

Output review and escalation: the bank reviews delivered outputs and escalates when standards are not met. The provider corrects.

The bank does not need an internal project manager for the implementation, or need IT resources for integration work. The start-to-result timeline is weeks, not months.

Example: A $600M Community Bank, No New Hires, No New Systems

A $600M community bank had a loan operations team spending approximately 40% of its time on document preparation before underwriting could begin. The team was not the bottleneck because they were slow. They were the bottleneck because the volume of incoming commercial loan packages had grown faster than the team's capacity to process them manually. The bank engaged a managed loan document processing service. The scope was defined in two discovery sessions: commercial loan packages only, 15 document types, LOS output in a defined field format, 95% accuracy standard, 24-hour turnaround on complete packages. The delivery team was approved before going live. Onboarding took 18 days.

After the first month, the loan operations team's time on document preparation dropped from 40% of capacity to approximately 8% (exception review only). Loan cycle time from application to underwriting review dropped by four business days on average. The bank hired no new staff and implemented no new software.

Frequently Asked Questions

Does the managed service model work if our core system is legacy and has no APIs?

Yes. Managed back-office services typically operate on file-based data exchange rather than API integration. The core exports scheduled reports or flat files that the provider ingests. Processed outputs return in formats the core accepts through existing import processes. No API development is required, and the core system is not modified. This is one of the primary reasons the managed service approach works for community banks whose core providers have limited integration flexibility.

What happens to our process documentation if we end the engagement?

A well-structured engagement agreement specifies that all process documentation developed during the engagement belongs to the bank. The provider builds the documentation as part of onboarding. The bank retains it regardless of how the relationship ends. This is an important negotiating point before the engagement begins, not a question to address after the contract is signed.

How is data security handled when an external provider processes our loan documents?

Data security for managed back-office engagements is an operational and contractual question. The relevant controls include: document transmission through secure channels (SFTP or encrypted upload), access limited to the specific documents and data required for the defined function, processing in a SOC 2 certified environment, confidentiality agreements covering all team members who handle the data, and clear data retention and deletion policies. Shore Group holds SOC 2 Type I certification.

Can we start with one workflow and expand later?

Yes, and this is the recommended approach. Starting with one well-defined workflow allows the bank to evaluate the delivery quality and working relationship before expanding scope. The Pilot-to-Partnership model is structured specifically for this: a defined pilot scope, a fixed-rate pilot period, and expansion only after the bank has seen the output quality and confirmed the relationship works. Adding a second workflow after the first is running well is typically faster to onboard because the provider already understands the bank's data environment and documentation standards.

What if our volume is too small to justify a dedicated managed service?

Managed back-office services scale to volume. A community bank processing 20 commercial loan packages per month has a different starting point than one processing 200. For lower-volume functions, the engagement may start with a part-time allocation rather than a dedicated full-time professional. The provider's pricing model should reflect actual volume rather than charging for capacity the bank does not use. If a provider requires minimum volume commitments significantly above your current level, that is a sign the model is not calibrated for your scale.

Shore Group manages back-office workflows for community banks

Document processing, reconciliation, compliance data aggregation, and exception handling — with no software to implement and no headcount to add.

Our Approach