KYC Automation for Community Banks: From Manual Verification to Managed Workflow

Manual KYC is a document chase. Here is what a managed workflow does differently — and why it matters for examiners.

TL;DR

Manual KYC is a document chase. Onboarding documents arrive from multiple channels, compliance officers copy data between systems, watchlist screens run one by one, and audit trails live in email threads and spreadsheets. A managed KYC workflow replaces that process with automated document collection, AI-powered data extraction, integrated watchlist screening, and exception-only routing to compliance staff. Faster onboarding, stronger documentation, and less skilled analyst time spent on low-value tasks.

The compliance burden at community banks is not proportional to their size. It is proportional to their transaction volume and customer base, which means the regulatory workload scales with growth while the compliance team often does not. According to FDIC data cited in a March 2026 analysis by TIMVERO, compliance expenditure represents 8.7% of non-interest expenses at small institutions compared to 2.9% at large ones. The same regulation imposes three times the proportional cost on a community bank that it does on a major national institution.

KYC is one of the most resource-intensive parts of that compliance burden. Every new commercial relationship, every account opening, every periodic review of an existing customer, and each one triggers a process that, at most community banks, is still largely manual. Documents arrive by email or through a portal. A compliance analyst reviews each one, copies data into the core or CRM, verifies beneficial ownership, runs watchlist checks, and chases anything that is missing.

That process is not going away. What can change is how much of it requires a compliance analyst's time and judgment, and how much can be handled by a workflow that is faster, more consistent, and better documented.

What Manual KYC Actually Looks Like at a Community Bank

The friction in manual KYC is not primarily about any single step. It is about the cumulative effect of many small inefficiencies compounding across every onboarding event.

A new commercial borrower submits onboarding documents. Some arrive by email, some through the bank's portal, and occasionally some by fax. The compliance analyst opens each one, determines what it is, extracts the relevant data fields, and enters them into the core system or a separate compliance platform. Beneficial ownership documentation requires identifying every individual who owns 25% or more of the entity and running each one through watchlist screening. If any document is missing, incomplete, or unclear, the analyst sends a follow-up request and waits.

The entire process for a straightforward commercial relationship can take anywhere from a few days to two or three weeks. For complex entities with multiple beneficial owners, international components, or incomplete documentation, it takes longer. And the audit trail for all of it lives in email threads, manual entries in multiple systems, and spreadsheets that are not connected to each other.

When an examiner reviews KYC documentation, they are not just asking whether the verification was done. They are asking whether it was done consistently, whether every step is documented with a timestamp and an identifiable reviewer, and whether the bank could reconstruct the process for any customer file on demand. Scattered email threads and manual spreadsheet entries are a documentation risk regardless of whether the underlying decisions were correct.

Why KYC Complexity Is Growing for Community Banks

The regulatory environment around customer due diligence has become more demanding, not less. Two developments in particular have added to the KYC workload at community banks in ways that manual processes struggle to absorb.

#1 FinCEN's Customer Due Diligence Rule and beneficial ownership

FinCEN's CDD Rule requires banks to identify and verify the beneficial owners of legal entity customers, specifically any individual who owns 25% or more of the entity or exercises significant control. For a straightforward single-owner business, this is manageable. For entities with layered ownership structures, multiple controlling parties, or foreign components, the verification process is substantially more complex.

The compliance team at a community bank handling commercial relationships must collect ownership documentation, verify each beneficial owner's identity, screen each one against applicable watchlists, and document the entire process. When the entity structure changes, that process repeats. Keeping beneficial ownership records current across a commercial loan portfolio is an ongoing operational task, not a one-time onboarding activity.

#2 Rising examiner expectations on documentation quality

Enforcement activity in the banking sector has made examiners more attentive to KYC documentation quality, not just KYC completion. The TD Bank case resulted in a $3.09 billion penalty (the largest AML-related fine in US banking history) centered in part on systemic failures in customer due diligence and monitoring. While the scale of those failures far exceeds what a community bank would face, the regulatory direction it signals is clear: documentation gaps and process inconsistencies are examination risks regardless of institution size.

Examiners increasingly expect not just that KYC was performed but that it was performed consistently, documented contemporaneously, and is fully retrievable. This expectation intersects directly with data lineage and audit readiness. Banks that cannot demonstrate a complete, traceable record of their KYC process for any given customer file are exposed, even when the underlying decisions were sound.

What KYC Automation Means in Practice

Automating KYC does not mean removing compliance judgment from the process. It means removing the low-value manual work that precedes that judgment, so analysts spend their time on decisions rather than document assembly.

A managed KYC workflow operates across four stages, each of which reduces manual handling while maintaining full regulatory defensibility.

#1 Document collection and intake

Rather than documents arriving piecemeal through email and portals, a managed workflow centralizes intake from any source. Documents are received, logged with a timestamp and source record, and immediately checked against a required document checklist for that customer type. Missing items are flagged automatically and a request is sent without an analyst having to track what is still outstanding. The collection stage is complete when all required items are present and accounted for, not when someone remembers to follow up.

#2 Classification and data extraction

Each document is classified by type: government-issued ID, corporate formation document, beneficial ownership certification, financial statement, or other required item. Data fields are extracted automatically: name, date of birth, identification numbers, ownership percentages, entity type, jurisdiction of formation. For documents in foreign languages, extraction occurs in the source language with translation applied to structured output fields.

The extraction output is a structured dataset, not a collection of PDFs. That dataset feeds directly into the compliance platform or core system, eliminating manual data entry and the transcription errors that come with it.

#3 Watchlist screening and risk scoring

OFAC, PEP, and adverse media checks run automatically against every beneficial owner and key entity identified in the documentation. Results are categorized: clear non-matches, potential matches requiring review, and confirmed matches requiring escalation. The risk tier assigned to the customer relationship is updated based on screening results and entity characteristics. All of this happens without an analyst manually entering names into a screening system and recording the results.

#4 Exception routing with context assembled

Genuine exceptions (potential watchlist matches, incomplete beneficial ownership chains, and documentation that does not reconcile with stated entity structure) route to the compliance analyst with all relevant documents, extracted data, screening results, and flagged discrepancies already assembled. The analyst reviews evidence and makes a decision. This is the human-in-the-loop model applied to compliance onboarding: automation handles the volume and the assembly work, humans handle the judgment. The analyst is not starting an investigation from scratch. They are reviewing a complete case file.

What the Audit Trail Looks Like

The documentation output of a managed KYC workflow is fundamentally different from manual documentation in one critical way: it is contemporaneous by design rather than reconstructed after the fact.

Every step in the workflow produces a logged record: document received, timestamp, source. Document classified as type X, confidence score Y. Data fields extracted, values recorded. Watchlist screen run, results stored. Exception routed to analyst Z, decision recorded, timestamp. The complete record for any customer file is assembled automatically as the workflow runs, not assembled manually before an examination.

When an examiner asks to see the KYC file for a specific commercial customer, the response is minutes rather than days. The entire process history is available, traceable to individual steps, and not dependent on any single employee's memory of what they did.

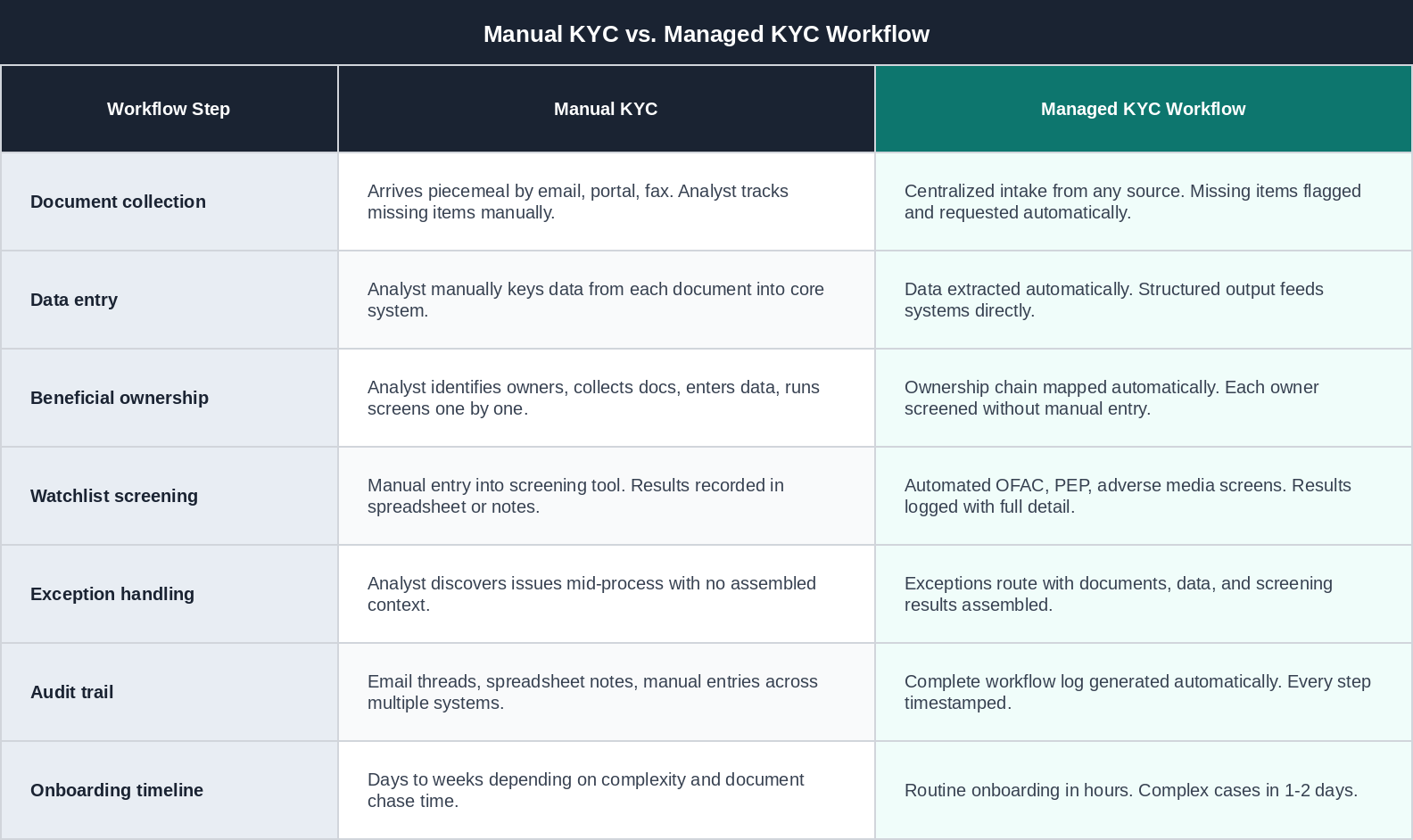

Manual KYC vs. Managed KYC Workflow

Example: A $650M Community Bank Onboards a New Commercial Relationship

A commercial borrower is a real estate investment entity with four beneficial owners, two of whom are foreign nationals. The entity has subsidiaries in two states and one foreign jurisdiction. Under a manual process, this onboarding takes the compliance team approximately twelve business days: collecting formation documents from multiple jurisdictions, verifying four beneficial owners individually, running foreign PEP and adverse media checks that the standard screening tool does not cover automatically, and assembling a file that satisfies the examiner's expectation of completeness.

Under a managed KYC workflow, the required document checklist for a multi-jurisdictional entity is configured in advance. The intake system identifies which documents are present and which are missing within minutes of the initial submission. Formation documents from each jurisdiction are classified and data extracted. All four beneficial owners are screened automatically, including against international PEP databases. The two items that require genuine judgment (a partial name match on one beneficial owner's adverse media screen and an ambiguous ownership percentage on a subsidiary) route to the compliance analyst with the relevant documents and screening detail already assembled. The analyst resolves both items the same day. Total elapsed time: two business days.

What KYC Automation Does Not Replace

Being precise about the boundaries of automation matters as much as describing its capabilities. Several elements of KYC remain squarely within compliance analyst responsibility regardless of how the workflow is structured.

Final disposition decisions on potential watchlist matches. Automation identifies and routes. An analyst decides.

Judgment calls on complex ownership structures that do not fit standard patterns. Automation handles defined structures. Novel or ambiguous structures require human interpretation.

The bank's BSA/AML policy and risk appetite. Automation executes the bank's defined process. The process design and risk thresholds remain the bank's responsibility.

Ongoing monitoring decisions for high-risk relationships. Automation can flag trigger events for review. The bank's compliance team determines how to respond.

Automation changes what the analyst spends their time on, not whether they are involved. The goal is to concentrate compliance expertise on decisions that require it, not to substitute automation for compliance judgment.

Frequently Asked Questions

Does KYC automation satisfy regulatory requirements on its own?

Automation is a delivery mechanism for a KYC program, not a replacement for one. FinCEN's CDD Rule, BSA requirements, and examiner expectations require that the bank has a risk-based KYC program with documented policies, appropriate oversight, and evidence of consistent execution. A well-configured managed KYC workflow produces the documentation and consistency that satisfies those requirements. But the bank's compliance team remains responsible for the program design, the risk thresholds, and the final decisions on exceptions. Automation that runs without a sound underlying program does not satisfy the regulatory requirements.

What happens when automated screening flags a false positive?

False positives (potential watchlist matches that turn out not to be the subject of concern) are a normal feature of any screening program. The managed workflow routes these to a compliance analyst with the relevant screening detail assembled: the name match, the source of the entry, the entity or individual's identifying information, and any available distinguishing data. The analyst reviews and documents a determination. That determination becomes part of the permanent KYC file. False positives that are correctly cleared with documented rationale are not an examination risk. False positives that are cleared without documentation are.

Can KYC automation handle international customers and foreign beneficial owners?

Yes, with some important qualifications. Automated extraction handles documents in multiple languages, and watchlist screening can be configured to include international PEP databases, sanctions lists from multiple jurisdictions, and adverse media sources in multiple languages. The qualification is that highly complex cross-border ownership structures may still require experienced compliance analyst judgment at points in the process where the automation encounters configurations it was not designed to handle. The workflow should be designed to route those cases appropriately rather than process them automatically.

How is beneficial ownership handled when entity structure changes?

A managed KYC workflow can be configured to trigger a beneficial ownership review when defined events occur: a change in entity registration, a significant transaction involving the entity, a periodic review date, or a flag from ongoing monitoring. When the trigger fires, the workflow initiates a new verification sequence for the updated ownership information using the same automated process as initial onboarding. The result is a current beneficial ownership record that is maintained systematically rather than allowed to become stale between manual reviews.

Is the bank still responsible for KYC decisions made within an automated workflow?

Yes, fully. The bank's compliance program is the bank's responsibility regardless of how it is executed. Regulators examine whether the bank's KYC decisions were appropriate, documented, and consistent with the bank's stated policies. A managed workflow that produces consistent, well-documented decisions supports that examination. The bank owns the policies, the risk appetite, and the final decisions on exceptions. The managed service executes the defined process and produces the documentation. Responsibility for the program does not transfer to the service provider.

Ready to Transform Your KYC Process?

Shore Group manages KYC workflows for community banks - from document collection, classification, beneficial ownership verification, watchlist screening, and exception routing — with SLA-backed accuracy and exam-ready documentation.

Learn How We Work